What Is a Fiduciary Financial Advisor? Everything You Need to Know

Most people assume every financial advisor is required to put their clients first.

Surprisingly, that’s not always the case.

Some financial advisors are legally required to act in your best interests. Others are only required to recommend investments or strategies that are considered suitable for your financial situation. While that distinction may seem subtle, it can have a meaningful impact on the advice you receive, the fees you pay, and ultimately your long-term financial future.

That’s where a fiduciary financial advisor is different.

A fiduciary financial advisor is legally obligated to prioritize your best interests over their own. This fundamental distinction sets them apart from other financial professionals and is a crucial factor to consider when choosing someone to entrust with your financial future.

The term “fiduciary” is not merely industry jargon; it represents a legal standard with significant implications. For individuals planning their retirement, managing their wealth, or establishing a lasting legacy, comprehending this distinction is of utmost importance.

What Does “Fiduciary” Actually Mean?

A fiduciary is any individual or organization legally obligated to prioritize someone else’s interests over their own. In the realm of financial advising, this entails that your advisor should make recommendations that genuinely align with your best interests, regardless of commission rates, sales quotas, or the benefits provided by a third-party partner.

Fiduciary advisors are bound by two foundational duties:

- Duty of care – Before making any recommendation, a fiduciary must thoroughly research all available options and identify the one most likely to serve your interests.

- Duty of loyalty – A fiduciary cannot use their position to benefit themselves at your expense. Your goals come first.

These aren’t professional courtesies. They’re legal obligations. A breach of fiduciary duty carries real consequences: financial, professional, and legal.

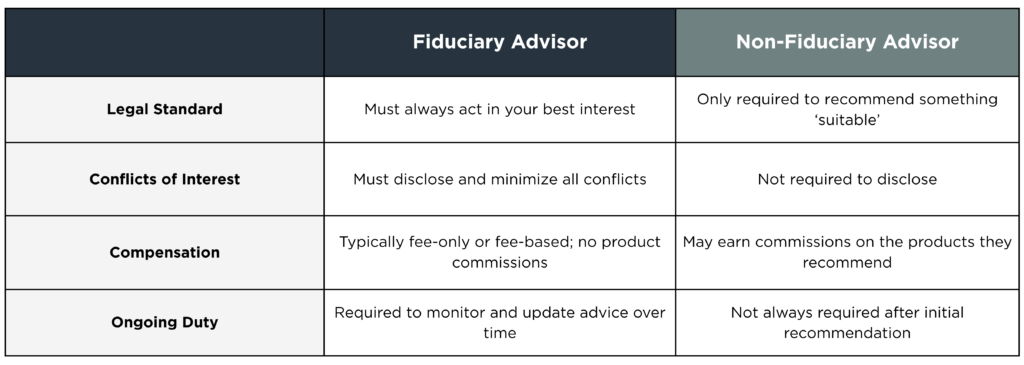

Fiduciary vs. Non-Fiduciary: What’s the Real Difference?

Not every financial professional is a fiduciary. Many operate under what’s called the “suitability standard”, a rule that only requires their recommendations be suitable for you, not necessarily the best option available.

That gap is more significant than it appears. An advisor operating under the suitability standard could recommend a product that generates higher commissions, provided it’s technically suitable for your circumstances. They may be obligated to inform you about a better, more cost-effective alternative. They’re not required to monitor your plan over time. Additionally, they don’t have to disclose conflicts of interest in the same manner as a fiduciary.

Here’s how the two standards compare:

Working with a fiduciary doesn’t guarantee perfect outcomes. Markets fluctuate, circumstances change, and no advisor can control the future. However, it does ensure that every recommendation you receive prioritizes your interests above all else. This meaningful foundation is essential for any long-term financial relationship.

Who Is Required to Act as a Fiduciary?

Some financial professionals are fiduciaries by designation. Others choose to hold themselves to that standard voluntarily. A few common examples:

- Registered Investment Advisors (RIAs) – Required under the Investment Advisers Act of 1940 to uphold fiduciary duty with clients.

- Certified Financial Planners (CFPs) – The CFP Board requires all designees to operate as fiduciaries as part of their code of conduct.

- Accredited Investment Fiduciaries (AIFs) – Individuals must adhere to fiduciary standards and engage in continuous professional development to retain their designation.

Titles like “financial advisor”, “wealth manager”, or “financial consultant” aren’t regulated the same way. A professional using those terms isn’t automatically a fiduciary so it is always worth asking directly.

We operate as an independent, fee-based registered investment advisor. This means that fiduciary duty is not merely a stated value but is embedded in our structure and registration.

How to Tell If Your Financial Advisor Is a Fiduciary

The simplest approach? Ask them directly. “Are you a fiduciary?” is a reasonable, professional question. Their answer, and how they answer it, will tell you a lot.

A few other ways to verify:

- Look at how they’re compensated. Fee-only advisors earn no commissions on the products they recommend, which removes one of the most common conflicts of interest. If an advisor is commission-based, ask how they handle potential conflicts when they arise.

- Check their credentials. CFP®, AIF®, and RIA designations generally carry fiduciary requirements. Look for those letters and verify them.

- Search public records. The SEC’s Investment Professional database and FINRA’s BrokerCheck allow you to confirm registration and review any disciplinary history before your first meeting.

- Ask about third-party verification. Some firms carry CEFEX certification, an independent, third-party assessment confirming adherence to fiduciary investment standards. It’s not common, and it’s a meaningful signal.

Why a Fiduciary Standard Matters for Retirement Planning

Retirement planning involves decisions that compound in both directions. A recommendation that prioritizes the advisor’s financial gain over your interests may appear insignificant in the initial year. However, over two decades of investment choices, fee structures, and plan modifications, even minor misalignments can significantly impact the outcomes.

This is especially true for:

- People nearing or in retirement, where the sequence of withdrawals, tax strategy, and investment mix all interact in ways that require careful personalized analysis.

- Business owners evaluating retirement plans options for themselves and their employees, where competing product incentives can cloud objective advice.

- Nonprofits, foundations, and endowments, whose boards carry fiduciary responsibilities of their own benefit from working with an advisor who understands that obligation.

For business owners, we specialize in company-sponsored retirement plans and wealth planning for business owners. For nonprofits and foundations, the stakes are equally high. The board owes a fiduciary duty to the mission. The advisor they choose should uphold that same standard. Our work with nonprofits is built around that alignment. Learn more about our approach to nonprofit investment management.

What a Fiduciary Relationship Looks Like at Petersen Hastings

We are an independent, fee-based Registered Investment Advisory firm, which means fiduciary accountability is woven into how we’re structured, it’s not a marketing position.

We also hold CEFEX certification, a third-party standard that independently verifies adherence to fiduciary investment practices. That kind of external validation is rare in this industry. It means the fiduciary commitment is verified, not self-reported.

Our client-centered discovery process, Your Invested Journey, was developed in collaboration with a psychologist to gain a deeper understanding of clients’ values, concerns, aspirations, and fears. This foundational knowledge shapes every plan we create. It’s crucial to recognize that an advisor’s legal obligation to prioritize your interests is paramount. However, what truly distinguishes a fiduciary relationship from merely being labeled as such is the advisor’s commitment to actively putting your interests first throughout their entire process.

Questions to Ask Any Advisor Before You Commit

Before working with any financial professional, there are several questions you should ask a prospective advisor. The answers will tell you more than any brochure.

- Are you a fiduciary, and if so, do you adhere to this standard consistently throughout our relationship, or only at specific points?

- Are you a fee-only advisor, or do you earn commissions on certain products you recommend?

- Do you hold any certifications, such as CFP®, AIF®, or RIA registration, that mandate a fiduciary standard?

- How do you handle situations where your compensation might conflict with my best interests?

- Has your firm or any of its advisors encountered regulatory action or disciplinary proceedings?

A good fiduciary advisor won’t hesitate on any of those. They’ve thought carefully about these questions, and they want you to ask them. Take note, this is a ‘yes’ or ‘no’ questions. Any response implying they are “like a fiduciary” should raise some concern.

Frequently Asked Questions

Is a fiduciary advisor more expensive?

Not necessarily. Fee-only fiduciary advisors are transparent about how they’re paid, typically through a flat fee, hourly rate, or a percentage of assets under management. Non-fiduciary advisors may appear less expensive upfront, but commissions on products they recommend can create hidden costs over time. Many clients find the total cost of working with a fiduciary is similar or lower once all fees are accounted for.

Can a financial advisor be a fiduciary only part of the time?

Yes, and this is worth asking about specifically. Some advisors operate as fiduciaries when providing investment advice, but not when selling certain insurance products or other commission-based offerings. Asking whether an advisor is a fiduciary “at all times” rather than just “in general” is a more precise way to understand their obligations.

What’s the difference between a fiduciary and a fee-only advisor?

“Fiduciary” describes a legal standard of care. “Fee-only” describes a compensation model. The two often go together, but they’re not the same thing. A fiduciary advisor who is also a fee-only receives no commissions from third parties, which removes one of the most common sources of conflict. It’s a combination worth looking for.

What happens if a fiduciary advisor breaches their duty?

A breach of fiduciary duty is a legal violation. Depending on the circumstances, clients may have recourse through civil litigation, regulatory complaints to the SEC or FINRA, or arbitration. Fiduciaries who knowingly or negligently act in their own interests rather than a client’s face financial, professional, and legal consequences.

Is Petersen Hastings a fiduciary?

Yes. Petersen Hastings is an independent, fee-based Registered Investment Advisory (RIA) firm, which carries a fiduciary obligation under federal securities law. The firm also holds CEFEX certification, an independent, third-party verification of fiduciary investment practices. Our advisors are legally and professionally required to always act in the clients’ best interests.

Ready to invest in what matters to you? Call today or schedule a free consultation with your local Advisor.